Ivaylo Naydenov holds a Master's degree in Nuclear Power Engineering and a PhD in Nuclear Power Installations and Systems from the Technical University - Sofia. He has worked as an editor in the "Power Engineering" section of the “Utilities” magazine and in the field of energy trading. In the period 2014-2019 he held successively the academic positions of "Assistant Professor" and "Principal Assistant Professor” in the Department of “Thermal Power Engineering and Nuclear Power Engineering" at the Technical University - Sofia. He has short-term specializations in the field of energy security (NATO School in Antalya, Turkey, 2015 and Masaryk University School, Brno, Czech Republic, 2016) and critical raw materials (COST Action, Higher Technical Institute, Lisbon, Portugal, 2017). He has undergone numerous trainings in energy management, energy markets and energy diplomacy. He won first place in the Best Young Scientist competition of the Bulgarian Nuclear Society in 2017. He holds the position of Executive Director of the Bulgarian Federation of Industrial Energy Consumers (BFIEC) since October 2019.

At the end of August, the heat is not only on the beaches, but also on the energy markets.

Electricity has been posting peak after peak with daily prices on the day-ahead segment of the IBEX exceeding 1100 BGN/MWh. These peaks are driven by high gas prices in European markets as well as the drought in Western Europe, which has led to capacity outages and fuel transportation difficulties. The high prices in Bulgaria are also dictated by the connectivity of the EU markets.

Gas prices at the Dutch trading point TTF reach levels of around 270-280 EUR/MWh. Similar values mark the futures contracts for the coming months. What began as an uptrend in prices in late summer last year, fueled by then-low levels of European gas storage fills, has turned into a price shock underpinned by geopolitical factors, supply risks to the European Union and a general deficit of gas worldwide.

The sharp jump in gas prices was inevitably felt in our country, especially after the lost quantities under the contract with Gazprom Export. Thus, the price of gas sold by Bulgargaz EAD to consumers directly connected to the gas transmission network rose from 142.99 BGN/MWh in April to 298.29 BGN/MWh in August. The requested price for September is 315 BGN/MWh.

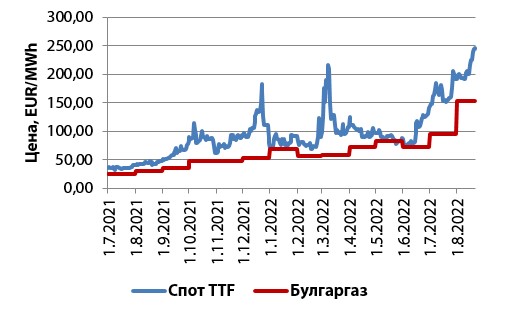

The dynamics of TTF spot prices and Bulgargaz monthly prices for the period July 1, 2021 - August 22, 2022 are illustrated in Figure 1.

Figure 1. Development of natural gas prices at the TTF and Bulgargaz trading point for the period July 1, 2021 - August 22, 2022.

It can be seen that during most of the considered period, Bulgargaz prices were relatively stable, but protected from the volatility of the spot market. This is because the price formula of gas supplies from Azerbaijan is tied to the prices of alternative fuels (the so-called "oil-indexed component"), as well as the presence of a similar component in Gazprom's gas pricing. In the last two months, a sharp jump in the price of gas supplied by Bulgargaz has been observed due to the increase in the share of gas quantities purchased at close to spot prices. The price of Bulgargaz is lower than the full spot price, as there are still supplies in the gas mix at prices linked to the prices of alternative fuels, which are currently more profitable. This circumstance, however, is not reassuring, since for the period July 1, 2021 - August 1, 2022, the price of gas has increased 6 times - from 49.94 BGN/MWh for July 2021 to 298.29 BGN/ MWh for August 2022.

How do these prices affect energy-intensive industries?

They are characterized by a relatively large share of energy costs in processing costs – sometimes this share exceeds 60%. In most cases, the increase in energy prices cannot be directly passed on to the end customer. Therefore, the uncontrollable increase in energy prices leads not only to a loss of competitiveness, but also threatens the economically justified operation of the respective enterprise. Such industries are ferrous and non-ferrous metallurgy, glass production and ceramics, nitrogen-fertilizer and chemical industry, mining of metal minerals, cement production, etc.

What should be done?

For electricity prices, however, a compensation mechanism for non-domestic consumers was introduced from the end of 2021, which, with various modifications, is still operating and is scheduled to operate until the end of 2022. Since there is no prospect of the price situation normalizing, it is necessary to think about what actions will be taken after January 1, 2023.

The continuation of the compensatory mechanism in one form or another is possible, but additional actions may also be taken. Such could be the solution to the problem with the excessive share of the spot market in electricity trade in our country through the development of trade with long-term contracts. Another possible solution is defending before the European Commission a temporary mechanism for two-level pricing on the market - separately for the domestic and foreign markets. Such an approach was successfully defended by Spain and Portugal, and currently prices for end users there are several times lower than those in the rest of the EU.

With regard to natural gas, it is extremely imperative to find a long-term solution to ensure supplies at an acceptable price, to put the Komotini-Stara Zagora interconnector into commercial operation as soon as possible, which will further lower the price of Azeri gas, as and "Bulgargaz" to notify its customers as a matter of urgency whether it will offer them supply contracts in the coming year, or whether consumers should look for alternative suppliers.